The Singapore condominium resale market has seen a dynamic October, marked by a rare price dip yet coupled with a notable rise in transaction volumes. With expert insights, emerging trends, and projections for 2025, this article examines the evolving landscape of Singapore’s condo resale market and its implications for buyers, sellers, and investors.

October Highlights: A Mixed Bag of Trends

First Price Decline in 10 Months

For the first time in 2024, condo resale prices registered a 0.5% dip month-on-month, as reported by SRX and 99.co. This decline was largely driven by the Rest of Central Region (RCR), which saw prices fall by 0.8%. In contrast:

- Core Central Region (CCR): Prices increased by 0.5%.

- Outside Central Region (OCR): Prices rose by 1%.

Despite the monthly contraction, year-on-year figures paint a more positive picture:

- CCR prices are up 3.7%.

- RCR prices have risen 3.3%.

- OCR prices are 3.9% higher.

The last recorded decline before this was in December 2023, underscoring the rarity of such dips.

Surge in Transaction Volumes

While prices fell, resale volumes surged by 8.1% from September, with 1,124 units transacted in October. This marks a 29.1% increase year-on-year and an 11.3% rise above the five-year October average. Analysts attribute this activity spike to factors such as:

- Interest rate cuts: The U.S. Federal Reserve’s recent reductions have led to a moderation in Singapore’s three-month SORA, dropping from 3.54% in mid-September to 3.25% by November 25. This has made home loans more attractive.

- Demand from HDB upgraders: According to URA Realis data, 331 units in October were purchased by HDB upgraders, representing a 5.8% month-on-month increase.

Factors Influencing the Market

New Supply Impact

The dip in prices is largely attributed to an influx of newly completed units:

- 3,225 non-landed units obtained Temporary Occupation Permits (TOP) in Q3 2024, the highest quarterly number this year.

- This follows the record 4,036 units completed in Q4 2023.

According to Mohan Sandrasegeran, head of research at Singapore Realtors Inc, this surge in supply has eased pressure on resale prices.

Demand Shifts to New Launches

November saw several high-profile project launches that attracted significant interest, diverting attention from the resale market. Christine Sun, chief researcher at OrangeTee, expects this trend, combined with year-end festivities, to soften resale activity further in November and December.

Regional Insights and Notable Transactions

Regional Breakdown

- OCR (Outside Central Region): Leading the market, OCR accounted for 50% of transactions, driven by demand from HDB upgraders.

- RCR (Rest of Central Region): Contributed 31.1% to total sales, despite the monthly price dip.

- CCR (Core Central Region): Represented 18.9% of transactions, with sustained demand from higher-end buyers.

Record-Setting Transactions

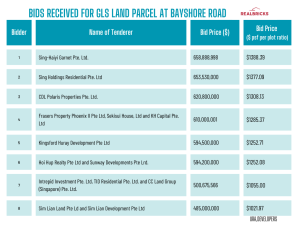

The most expensive resale unit in October was a $14.1 million condo at Cuscaden Reserve. Meanwhile, District 20 (Ang Mo Kio/Bishan/Thomson) recorded the highest median capital gain at $650,000, reflecting its strong investment potential.

Looking Ahead: Trends and Forecasts for 2025

Moderation in Supply

The pipeline of private home completions is expected to shrink significantly in 2025:

- A projected 41.3% decrease, with only 5,348 units set to obtain TOP.

This reduction in supply is anticipated to tilt the market balance in favor of sellers, with Christine Sun predicting a steady rise in resale prices as demand outstrips supply.

Price Gap Between New and Resale Properties

The growing price differential between new launches and resale condos is another key trend to watch. As developers price new projects higher, resale properties could become a more attractive option for budget-conscious buyers.

Sustained Demand from Upgraders

HDB upgraders are expected to remain a cornerstone of resale demand, bolstered by their confidence in long-term property investments.

Actionable Takeaways for Buyers, Sellers, and Investors

- For Buyers:

- Take advantage of current price moderation, especially in the RCR.

- Monitor interest rate trends, as further reductions could enhance affordability.

- For Sellers:

- Capitalize on high transaction volumes to secure quick sales.

- Consider listing properties in high-demand areas like the OCR or District 20 for better returns.

- For Investors:

- Focus on regions with strong capital gains potential, such as District 20.

- Stay updated on new launches and their impact on the resale market.

Conclusion

The Singapore condo resale market continues to navigate a complex interplay of supply, demand, and macroeconomic factors. While October’s price dip signals short-term adjustments, the longer-term outlook points to renewed growth driven by diminishing supply and robust demand. For those looking to buy, sell, or invest, staying informed and strategic will be key to capitalizing on the opportunities ahead.